Table of Contents

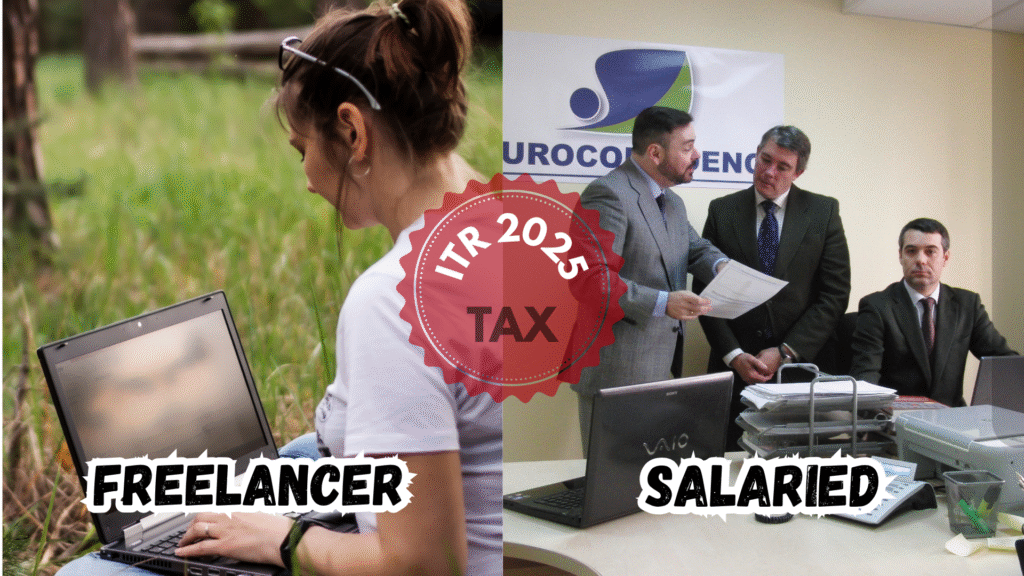

In the 2025–26 assessment year (FY 2024–25), freelancing and salaried income are treated very differently in India, especially when it comes to ITR filing, applicable forms, tax regimes, and compliance. Here’s a professional, practical, and up-to-date guide to help you navigate the system.

1. Income Classification — Business vs. Salary

Salaried Individuals: Income from salary is reported under “Income from Salaries,” typically backed by Form 16 issued by the employer, and the tax is deducted at source (TDS) before salary is paid. Source – The Economic Times.

Freelancers / Self-Employed: Freelance income is classified as “Profits and Gains of Business or Profession,” not salary

2. Choosing the Right ITR Form – ITR 2025

| Source of Income | Recommended ITR Form | Notes |

|---|---|---|

| Salary only (and up to ₹50L) | ITR-1 (Sahaj) | Suitable when salary, interest, LTCG (Section 112A), etc., only (The Economic Times) |

| Salary + Freelance/Profession | ITR-3 | Required if you maintain detailed books of accounts (TaxBuddy.com) |

| Freelance/Professional income, up to ₹50-75 L | ITR-4 (Sugam) | Under presumptive taxation (Section 44ADA for professionals) (CAclubindia) |

| Capital gains, foreign investments, no business income | ITR-2 | For non-business income along with salary (The Economic Times) |

3. Tax Regimes & Deductions

#Old Tax Regime:

Allows deductions like 80C (₹1.5 L), 80D, HRA, and standard deduction (₹50,000 or ₹75,000) in India.

#New Tax Regime:

Offers lower slab rates with fewer deductions. As of FY 2025–26, the exemption limit is ₹4 L for all individuals, and Section – 87A rebate stands at ₹60,000 for incomes up to ₹12 L.

Note: Please, be assured with Updated & authorised platform for your confirmation. We are not responsible for your loss.

Click Here – Tax Calendar

4. Deductions and Ease of Filing

- Salaried Individuals: Straightforward filing via Form 16. (Deductions) such as HRA, medical, and investments are available under the old regime. Extensive disclosures are now mandatory in ITR-1/ITR-4 Excel utilities for FY 2024–25.

- Freelancers: You may claim business expenses—like internet, software, travel, depreciation, etc.—under ITR-3. However, under presumptive taxation (ITR-4), 50% of gross receipts are deemed expenses no detailed accounting.

5. TDS, Advance Tax & GST — What Freelancers Need to Watch

- TDS on Freelance Services: TDS is applicable under sections like 194J, 194C, 194H, etc. Freelancers must reconcile TDS with Form 26AS in ITR 2025.

- Advance Tax: Freelancers must pay if TDS is insufficient; otherwise, interest on late payment applies. The TDS threshold rose from ₹30,000 to ₹50,000 in Budget 2025.

- GST Compliance: Mandatory if annual turnover exceeds ₹20 L (or ₹10 L in some states). Domestic clients—18% GST applies; export of services is zero-rated, but returns must still be filed.

6. New Codes for Digital Earners (ITR-2025 Update)

For AY 2025–26, new profession-specific codes were introduced in ITR-3 and ITR-4:

- Influencers: Code 16021

- F&O Traders: Code 21010

- Commission Agents / Betting: Code 21009

This ensures clearer classification but also introduces ambiguity, such as for influencers, whose work may not fit within Section 44ADA’s “Specified Profession”

7. Deadline & Compliance Tips

- Due Date: ITR 2025 deadline extended to September 15, 2025, for AY 2025–26.

- Form Verification: Post-filing, returns must be verified within 30 days; retain all documentation for future scrutiny.

- Avoid Mistakes:

- Use correct ITR form (don’t use ITR-1 for freelancers)

- Track and claim all eligible deductions

- Match income/TDS with Form 26AS

- Pay advance tax on time to avoid penalties

ITR-1 Exception For The Person Who –

(a) is a Director in a company

(b) has short term capital gain

(c ) has Long-term capital gain u/s 112A exceeding Rs.1.25 lakhs

(d) has held any unlisted equity shares at any time during the previous year

(e) has any asset (including financial interest in any entity) located outside India

(f) has signing authority in any account located outside India

(g) has income from any source outside India

(h) is a person in whose case tax has been deducted u/s 194N

(e) is a person in whose case payment or deduction of tax has been deferred on ESOP

(i) has any brought forward loss or loss to be carried forward under any head of income, (i) has total income exceeding Rs. 50 lakhs.

In Conclusion:

Process of ITR 2025 filing in FY-2025 requires clarity on income sources, applicable forms, tax regimes, and compliance rules. While salaried individuals benefit from simplicity and TDS support, freelancers must juggle accounting, GST, TDS, and advances albeit with greater potential deductions.